As mortgage rates continue to fluctuate, homebuyers are always looking for ways to save money when they can, especially on such a large investment. One way buyers can try to save some money is by purchasing mortgage points, also known as discount points. But what are they and how do mortgage points work? Let’s discuss.

Which Title Insurance Policy is Right for You? Learn More With This Chart

Mortgage Points Explained

Mortgage points are fees that you pay the lender to reduce the overall interest rate on your mortgage. These points are priced as a percentage of the cost of your mortgage and will reduce your interest rate by a certain amount. Buyers can choose to purchase mortgage points to lock in a lower interest rate and pay less on the loan over time. So, the more mortgage points purchased, the more you save on the interest rate of the loan.

How do Mortgage Points Work?

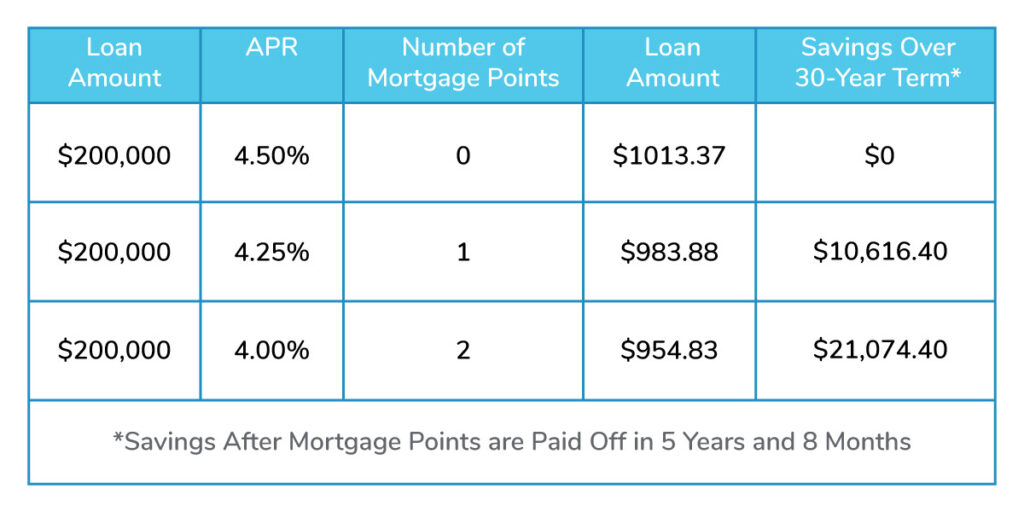

In the mortgage closing process, your lender may offer you the option of paying for points in exchange for paying down your interest rate. Each mortgage point costs 1% of the loan. So, 1 point on a $100,000 loan is equal to $1,000, 1 point on a $200,000 loan is $2,000, and so on. Lenders may also offer the option to buy point fractions such as ½ point for $500 on a $100,000 loan. These points then reduce your interest rate by a specific percentage and can vary from lender to lender. One lender may offer a 0.25% interest rate reduction for each point which can reduce the interest rate from 4.50% down to 4.25%. So, the more points, you purchase, the cheaper your interest rate.

While mortgage points decrease overall interest on your mortgage loan, it can also lead to increased savings over the course of the loan term. Since mortgage points decrease interest, points will also decrease your monthly mortgage payment.

For example, a 30-year mortgage loan of $200,000 with 4.5% interest will make the monthly payment $1,013.37. In this scenario, a mortgage point costs $2,000. If you purchase a single mortgage point at $2,000 in exchange for a 0.25% APR decrease, your monthly payment will then fall to $983.88. While that $29.49 savings may not seem like much, the cost of the mortgage point is paid off after 5 years, 8 months, and will save you $10,616.40 over the rest of the loan.

Is Purchasing Mortgage Points Right for You?

The decision to purchase mortgage points is up to the homebuyer and the plans for their home. Many buyers are reluctant to purchase points because they are unsure of how long they will remain in the home. With a little more investment at the beginning of the time in your home, you can save serious money over the course of the loan. To determine if mortgage points are right for you, it is best to crunch some numbers, assess your budget, down payment, and your future plans. If you plan on staying past your breakeven point, mortgage points can save you money in the long run when buying a home. No matter what your financial situation is, the team at Millennial Title is here to make the home buying process as easy as it can be. Contact our team today to learn more.